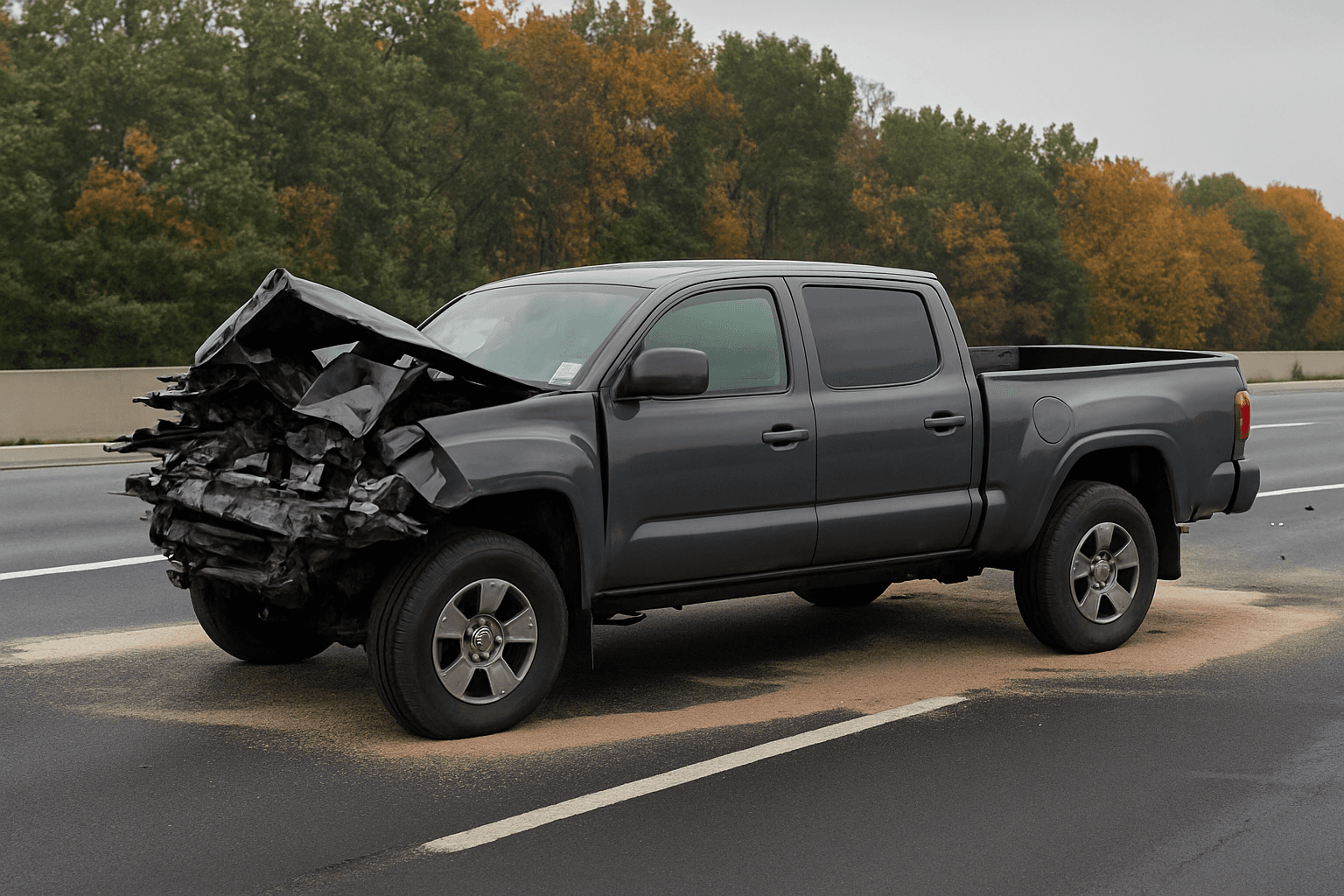

Single-vehicle accidents trigger carrier-specific surcharge tiers based on incident type—hitting a deer costs 9-13% more, but rollover or off-road events jump to 25-40% because insurers classify loss-of-control as predictive negligence.

How Carriers Price Single-Vehicle At-Fault Accidents

Carriers apply different surcharge tiers to single-vehicle accidents based on incident classification, not just fault status. A deer strike typically increases premiums 9-13% because it's coded as a comprehensive claim with limited negligence signal. A rollover or off-road crash jumps to 25-40% surcharges because carriers classify loss-of-control events as predictive markers for future at-fault multi-vehicle claims, regardless of whether another driver was present.

The distinction matters because your claims adjuster's incident report determines which tier applies. If you hit black ice and went into a ditch, the carrier codes it differently than if you overcorrected on a dry road and rolled the vehicle. Weather conditions, road surface, and your description during the first notice of loss call all feed the underwriting algorithm that assigns your post-accident pricing tier.

Most drivers assume single-vehicle accidents cost less than multi-vehicle claims. That's wrong for loss-of-control incidents. A rollover with $8,000 in damage and no other party can cost you more over 36 months than a $12,000 rear-end collision where you hit another car, because the rollover signals risk behavior that carriers weight heavily in renewal underwriting.

What Counts as At-Fault When No Other Driver Is Involved

You're at-fault in a single-vehicle accident if you filed a collision claim and your carrier paid for vehicle damage you caused by losing control, hitting a fixed object, or leaving the roadway. Comprehensive claims—deer strikes, falling tree branches, hail damage—don't trigger at-fault surcharges even if you're the only driver involved, because the loss isn't classified as driver negligence.

The coverage type under which your claim is filed determines fault classification. If you hit a guardrail and filed under collision coverage, it's at-fault. If a deer ran into your car and you filed under comprehensive, it's not. But if you swerved to avoid the deer, lost control, and hit a tree, the carrier codes it as at-fault collision because the impact resulted from your driving action, not the animal encounter itself.

Some states modify this framework. Michigan and a handful of no-fault states apply different surcharge rules to single-vehicle accidents depending on whether you triggered personal injury protection benefits or property damage only. In those states, a single-vehicle rollover with injuries can cost 50-70% more than the same crash with vehicle damage alone, because the combined claim crosses a higher underwriting threshold.

Find out exactly how long SR-22 is required in your state

Rate Increase Timeline After a Single-Vehicle Crash

Your current policy term continues at the existing rate until renewal, even after you file a single-vehicle at-fault claim. The surcharge appears at your next renewal date—typically 30-180 days after the accident depending on where you are in your policy cycle. Carriers don't apply mid-term increases for accident claims unless the incident also triggered a license suspension or multiple violations in the same event.

The 36-month surcharge clock starts on the accident date, not the renewal date when the increase first appears. If your accident was March 15, 2025, you'll see the surcharge at your next renewal, but it expires March 15, 2028 regardless of how many times you renew between those dates. Some carriers reassess at the 12-month and 24-month renewal marks, applying smaller incremental reductions if you maintain a clean record during the surcharge period.

Switching carriers before your renewal date doesn't avoid the surcharge. Your new carrier pulls a loss history report that shows the claim, and they price it into your quote. The only timing advantage to switching is if you can bind a new policy before your current carrier processes the claim into the national claims database—a window that typically closes 15-30 days after your first notice of loss.

Whether to File a Claim for Single-Vehicle Damage

File the claim if your vehicle damage exceeds twice your deductible and you're certain you'll keep the same coverage limits for the next 36 months. A $3,500 repair with a $500 deductible nets you $3,000 now but costs you $1,200-$2,400 in cumulative surcharges over three years at a 25% increase on a $400/month policy. The break-even point depends on your current premium and the incident type your carrier will assign.

Don't file if the damage is under $2,000 and you're already carrying violations or prior claims. Stacking a second at-fault event within 36 months can push you out of standard market access entirely, forcing you into non-standard carriers that cost 60-120% more than your current rate. The $1,800 you save by paying out of pocket preserves your underwriting tier, which protects you from the compounding cost of high-risk classification.

You have 24-72 hours to decide in most states. Carriers require prompt notification of accidents, but prompt means days, not hours. If you're unsure whether to file, report the accident to preserve your claim rights but don't request a damage estimate immediately. You can withdraw a claim before the carrier pays, but once they issue payment, the claim appears on your loss history even if you return the check.

How Single-Vehicle Accidents Affect Standard Market Access

One single-vehicle at-fault accident doesn't disqualify you from standard market carriers. Most major insurers allow one at-fault claim within 36 months before moving you to a higher-risk tier or non-renewing your policy. Two at-fault claims within 36 months crosses the threshold for most standard carriers, triggering non-renewal notices at your next policy term.

The exception is loss-of-control incidents combined with other risk factors. If your single-vehicle rollover also involved a DUI charge, suspended license, or serious injury, you'll move to non-standard or assigned risk markets immediately. Carriers treat combined violations and accidents as multiplicative risk, not additive.

Non-standard carriers like The General, Acceptance, and Bristol West accept drivers with multiple at-fault accidents, but they price policies 60-150% higher than standard market equivalents. If your current policy costs $180/month and you're facing non-renewal after a second accident, expect quotes in the $290-$450/month range depending on state and coverage limits. Non-standard coverage options remain available, but the price gap is significant.

Actions That Reduce Surcharge Impact in the Next 30 Days

Complete a state-approved defensive driving course before your renewal date if your state mandates point reduction or rate mitigation for voluntary course completion. Nine states—including California, Florida, and New York—require carriers to apply discount credits for defensive driving completion, which can offset 5-10% of your accident surcharge. The course must be completed before your renewal processes, not after the new rate takes effect.

Request a claims review if your accident involved weather, road defects, or mechanical failure you can document. Carriers allow claim reclassification in limited circumstances where third-party evidence supports non-negligent cause. A police report noting black ice, a repair invoice showing brake failure, or photos of road debris can move your claim from at-fault collision to comprehensive or no-fault, eliminating the surcharge entirely.

Increase your deductible to $1,000 or higher at renewal if you're facing a 25%+ surcharge and you have savings to cover future out-of-pocket costs. A higher deductible reduces your base premium by 15-25%, partially offsetting the accident surcharge and lowering your monthly payment even with the increase applied. This works only if you can afford the higher deductible on your next claim—don't trade immediate savings for unaffordable future risk.

What Your First Call to the Carrier Determines

Your description of the accident during first notice of loss shapes how the claim is coded, which determines your surcharge tier for the next three years. If you say "I lost control on a wet road," the adjuster codes it as driver error. If you say "I hit standing water and hydroplaned into the guardrail," it may code as weather-related with a lower negligence weight. The distinction is not dishonest—it's accurate framing of causation.

Don't speculate about fault or apologize during the initial call. Stick to observable facts: road conditions, weather, time of day, what you saw before impact. If the adjuster asks "Why do you think this happened," the correct answer is "I'm not sure—I'd like to wait for the police report and vehicle inspection before I speculate." Premature fault admission gets recorded in the claim notes and can't be retracted later.

Ask the adjuster how the incident will be classified before you authorize repairs. The coding decision happens within 48 hours of your first call, and once it's entered, changing it requires documented evidence and a formal review process most drivers never initiate. If the adjuster says it will be coded as at-fault collision, you still have the option to withdraw the claim and pay for repairs yourself if the math favors eating the cost.