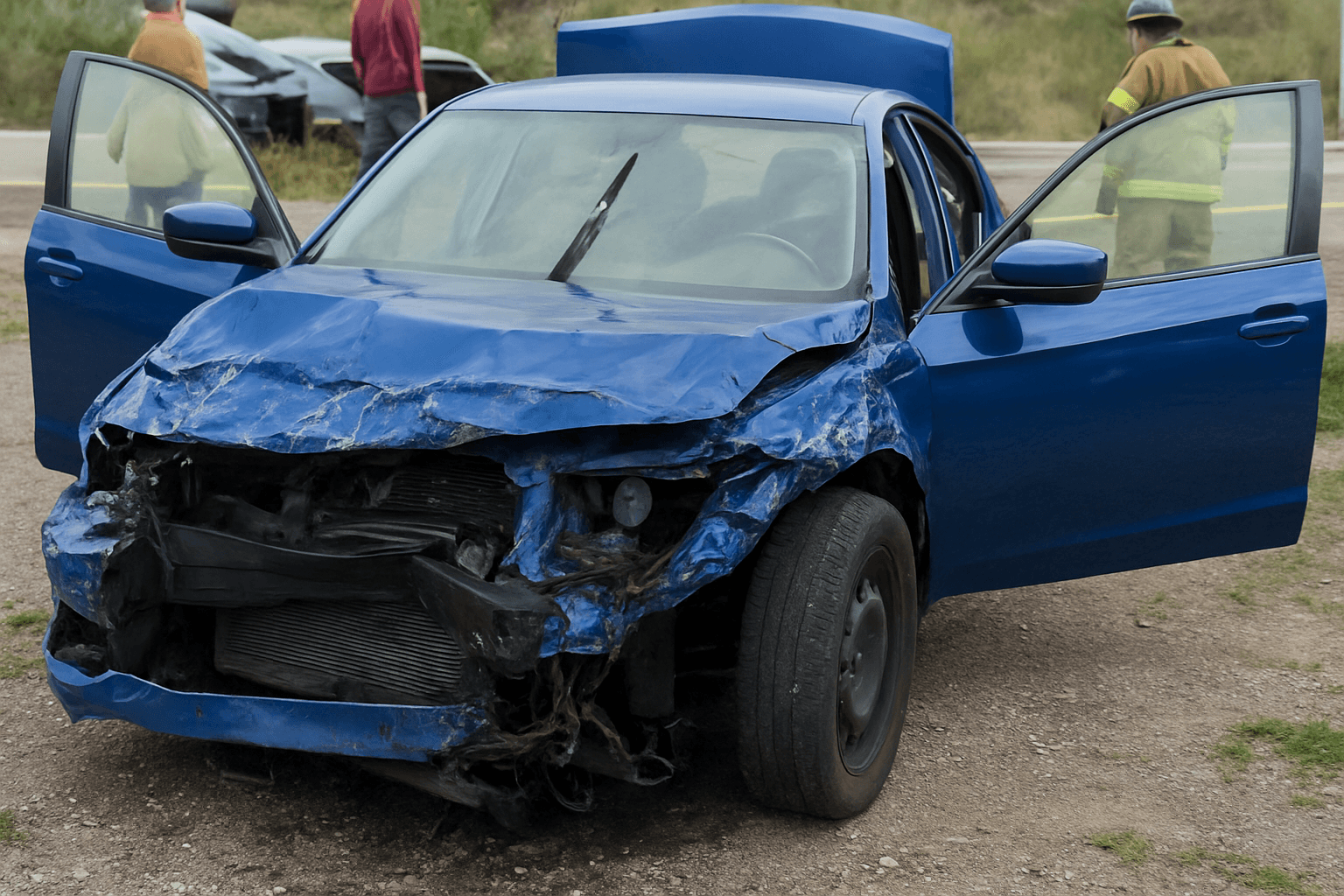

Property damage reporting thresholds vary by state, and failing to report a minor at-fault accident can trigger license suspension even when no one files a claim against you.

Which States Require Reporting for Property Damage Under $1,000?

Twenty-nine states mandate DMV accident reporting for property damage below $1,000, with thresholds ranging from $500 to $2,500 depending on jurisdiction. California requires reporting for damage exceeding $1,000 to any one party's property. Texas sets the threshold at $1,000 combined damage. Florida mandates reporting at $500 combined damage when the accident involves injury, death, or a vehicle towed from the scene.

The reporting obligation exists whether or not anyone files an insurance claim. You trigger the requirement by causing property damage above your state's threshold in a single incident, not by receiving a claim letter or police citation. Most drivers discover this requirement only after their license is suspended for non-compliance.

States with $1,000 or lower thresholds create the highest violation risk for minor parking lot collisions, scraped bumpers, and low-speed rear-end impacts where drivers exchange information and assume the matter is resolved. The DMV doesn't know you resolved it privately unless you file the mandated report within the statutory window.

What Happens If You Don't Report Within the State Deadline?

Most states impose a 10-day reporting deadline from the accident date, though some allow 15-30 days and others require notification within 72 hours if the accident involves specific criteria like injury or vehicle towing. Missing the deadline triggers automatic license suspension in 41 states, applied without prior warning or hearing.

The suspension persists until you file the overdue accident report and pay reinstatement fees ranging from $50 to $250 depending on state. Some states add a compliance filing requirement, mandating you maintain SR-22 insurance for 1-3 years after reinstatement even though the underlying incident was a minor property damage accident.

Carriers receive notification of the suspension when they pull your updated motor vehicle record at renewal or during routine monitoring. The suspension itself becomes a separate underwriting event, often triggering higher surcharges than the original at-fault accident because it signals compliance failure rather than driving error.

Find out exactly how long SR-22 is required in your state

Does Filing an Accident Report Guarantee Your Insurer Will Find Out?

Filing a state accident report does not automatically notify your insurance carrier, but it creates a state DMV record that appears on your motor vehicle report within 30-90 days. Carriers pull MVRs at policy renewal, after you file a claim, during new business underwriting, and periodically for existing policyholders in states that permit ongoing monitoring.

Some states cross-reference accident reports with active insurance policies and notify carriers directly when a policyholder files a report involving their insured vehicle. Most states do not. The timing gap between filing your report and your insurer discovering it depends on when your carrier next pulls your MVR.

If you file an insurance claim for the same incident, your carrier learns about the accident immediately regardless of whether you filed a state report. The claim triggers the underwriting review. If you don't file a claim and your state doesn't auto-notify insurers, the accident surfaces only when your carrier pulls your next MVR, which could be 6-12 months after the incident depending on your renewal date.

How At-Fault Property Damage Accidents Affect Your Rate

At-fault accidents with property damage typically increase premiums 20-40% at your next renewal, with the exact surcharge depending on your state's rating rules, your carrier's tier structure, and whether you have prior violations on record. A single at-fault accident moves most drivers from preferred to standard tier pricing, which persists for 3-5 years depending on state lookback windows.

Carriers apply accident surcharges differently than violation surcharges. An at-fault accident signals claims risk rather than unsafe driving behavior, so the increase reflects projected claim frequency and severity for drivers with your updated risk profile. States that prohibit surcharging below specific damage thresholds, like California's $1,000 minor accident threshold, prevent carriers from increasing your rate unless total property damage exceeds the state floor.

The rate impact intensifies if the accident triggers a license suspension for failure to report. The suspension appears as a separate line item on your MVR, coded as an administrative action rather than a moving violation. Carriers treat administrative suspensions as high-risk indicators because they demonstrate failure to meet legal compliance requirements, often adding 30-50% surcharges on top of the underlying accident penalty.

What You Should Do in the 72 Hours After a Minor At-Fault Accident

Confirm your state's property damage reporting threshold and deadline immediately after the accident. Check your state DMV website or contact your state Department of Motor Vehicles directly for the current threshold and required forms. Do not rely on the other driver's assessment of damage cost or their willingness to handle the matter privately.

File the required accident report within your state's deadline even if the other party says they won't file a claim and even if you plan to pay out of pocket. The reporting obligation is independent of claim filing and independent of fault admission. Most states provide online filing portals or accept mailed forms, but processing timelines vary.

Decide whether to file an insurance claim within 30 days of the accident. Filing a claim triggers immediate carrier notification and potential rate increases, but waiting risks discovering months later that the other party filed a claim against you after initially agreeing not to. If total damage exceeds your state's reporting threshold, you must file the DMV report regardless of your claim decision.