Pennsylvania carriers apply accident surcharges in two separate tiers based on claim payout — not just fault status. Here's what determines whether you face a 25% increase for three years or a 60% increase for five.

How Pennsylvania Carriers Price First At-Fault Accidents

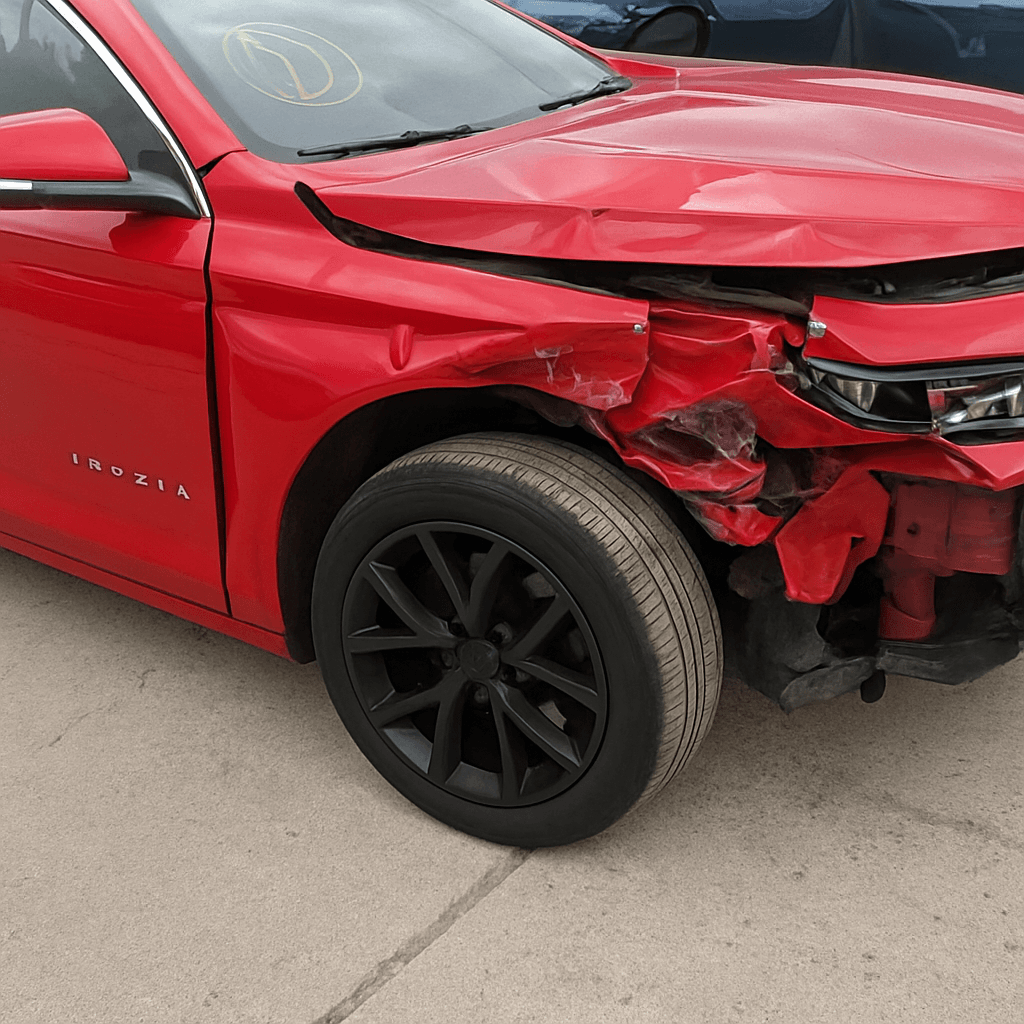

Your first at-fault accident in Pennsylvania triggers a surcharge between 20% and 75% depending on claim severity, not just fault determination. Carriers classify accidents into minor (property damage under $2,500 with no injuries) and major (property damage above $2,500 or any bodily injury claim) categories, applying separate surcharge schedules to each.

Minor accidents typically increase premiums 20-28% for 36 months from the accident date. Major accidents trigger 40-75% increases that remain until you complete your carrier's loss-free period definition, usually 3-5 years with no new claims. A fender-bender with $1,800 in damage costs you roughly $32-47 per month more on a standard policy. The same accident with a soft-tissue injury claim jumps to $68-126 per month more, even if the injury claim settles for under $5,000.

Pennsylvania permits accident forgiveness programs, but first-accident forgiveness only applies if you purchased it before the accident occurred. You cannot add forgiveness retroactively. Carriers offering voluntary forgiveness include State Farm, Progressive, Nationwide, and Allstate, with eligibility requiring 3-5 years of prior clean driving depending on the insurer.

What Moves an Accident from Minor to Major Surcharge Status

The difference between a 25% surcharge and a 65% surcharge comes down to three claim characteristics carriers evaluate within 90 days of the accident: total payout amount, presence of bodily injury claims, and whether the accident triggered a police report with specific violation codes.

Property damage claims under $2,500 with no injury typically stay in the minor tier. Once total payouts exceed $2,500 or any medical treatment is documented, most carriers reclassify to major tier pricing. This threshold applies to combined payouts — if you caused $1,400 damage to one vehicle and $1,300 to another, that $2,700 total moves you into major tier even though each individual claim stayed below threshold.

Police reports citing reckless driving, DUI, or excessive speed (20+ over) automatically trigger major tier classification regardless of payout amount. A $900 repair bill with a reckless driving citation prices the same as a $15,000 multi-vehicle collision for surcharge purposes. Carriers review the full accident file at your renewal — initial estimates matter less than final settlement amounts and police report narrative.

Find out exactly how long SR-22 is required in your state

When Your Rate Actually Increases After the Accident

Pennsylvania carriers apply accident surcharges at your next policy renewal, not immediately when the accident occurs. If your renewal date is 45 days after the accident, you see the increase in 45 days. If renewal is 10 months away, you have 10 months at your current rate before the surcharge applies.

Some carriers run mid-term re-underwriting if you file a claim exceeding $10,000 or involving serious injury. Mid-term re-underwriting can trigger a policy cancellation notice or immediate surcharge application with 30 days notice. This is rare for first accidents unless the claim involves multiple vehicles, significant injury payouts, or citation-level violations in the police report.

Your current insurer discovers the accident when you file the claim or when they pull your updated CLUE report at renewal. Shopping for quotes before your current carrier pulls that updated report preserves access to standard-market rates with new carriers who haven't yet seen the accident on your record. That window typically closes 60-90 days post-accident as CLUE databases update.

Whether Shopping After an Accident Saves Money

Switching carriers immediately after a first at-fault accident can reduce your total premium increase by 15-35% compared to staying with your current insurer, but only if you shop before your current policy renews. Carriers compete differently for one-accident drivers — some penalize first accidents heavily while offering better rates for clean records, others price one-accident risks closer to their clean-record base rates.

Progressive and Geico typically offer more competitive pricing for single-accident drivers compared to State Farm and Allstate, which apply steeper first-accident surcharges but offer accident forgiveness to long-term customers. USAA consistently prices first accidents lowest among major carriers but restricts eligibility to military members and families. Regional carriers like Erie and Penn National may offer better one-accident pricing than national carriers in Pennsylvania's southeastern and central regions.

Get quotes within 30 days of the accident, before your current renewal processes. New carriers see the accident on your application and price accordingly, but you avoid the compounding effect of your legacy carrier's surcharge plus limited competitive pressure. Drivers who shop immediately after a first accident pay an average $840-1,260 annually versus $1,080-1,680 for those who wait until after their surcharged renewal takes effect. Estimates based on available industry data; individual rates vary by driving history, vehicle, coverage selections, and location.

How Long Pennsylvania Accident Surcharges Stay on Your Rate

Minor accident surcharges expire after 36 months from the accident date with most Pennsylvania carriers. Major accident surcharges persist until you meet your carrier's loss-free period requirement, typically 3-5 years with no new at-fault claims, comprehensive claims above $1,000, or moving violations.

Your surcharge doesn't decline gradually — it drops to zero once you exit the lookback window. A driver surcharged 28% for a minor accident pays that 28% for 36 months, then returns to base rate on month 37 assuming no new claims. Carriers recalculate at each renewal, so the surcharge removal happens at your first renewal after the 36-month anniversary.

Some carriers extend lookback periods if you file additional claims during the surcharge window. A second at-fault accident within 36 months of your first restarts the clock on both accidents, creating a 6-year total surcharge period in some policy structures. Progressive and Nationwide apply cumulative lookback extensions; State Farm and Allstate typically run separate timelines per incident. Check your specific carrier's loss-free period definition in your policy declarations — this language controls when surcharges actually expire.

Actions That Reduce Rate Impact in the Next 30 Days

Complete a defensive driving course approved by PennDOT within 30 days of your accident. Pennsylvania allows a 5% rate reduction for voluntary defensive driving completion, applied separately from accident surcharges. The 5% discount doesn't erase your surcharge, but it reduces your new surcharged premium base. On a policy increasing from $140/month to $182/month post-accident, the defensive driving discount brings it to $173/month.

Shop for quotes before your current policy renews and before 60 days post-accident. Carriers pull updated loss reports at different intervals — some update CLUE within 30 days, others lag 90+ days. Early shopping captures quotes before all carriers see the accident, preserving access to better tier classifications with insurers who haven't refreshed your file yet.

Review your current coverage limits and deductibles before renewal. Increasing your collision deductible from $500 to $1,000 reduces your base premium 8-12%, partially offsetting the accident surcharge. Drivers paying $165/month pre-accident who face a 30% surcharge ($214/month) can move to $187/month by raising deductibles strategically. This only works if you can afford the higher out-of-pocket cost on your next claim.